來自:CFA > 2025 Level II > Quantitative Methods > Learning Module 3 Model Misspecification 2025-08-03 21:00

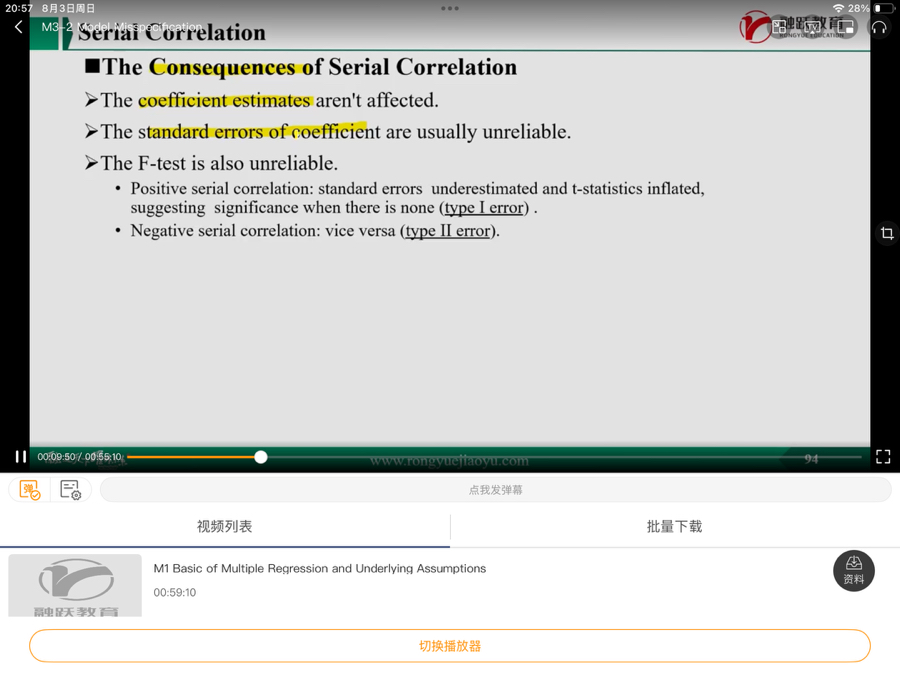

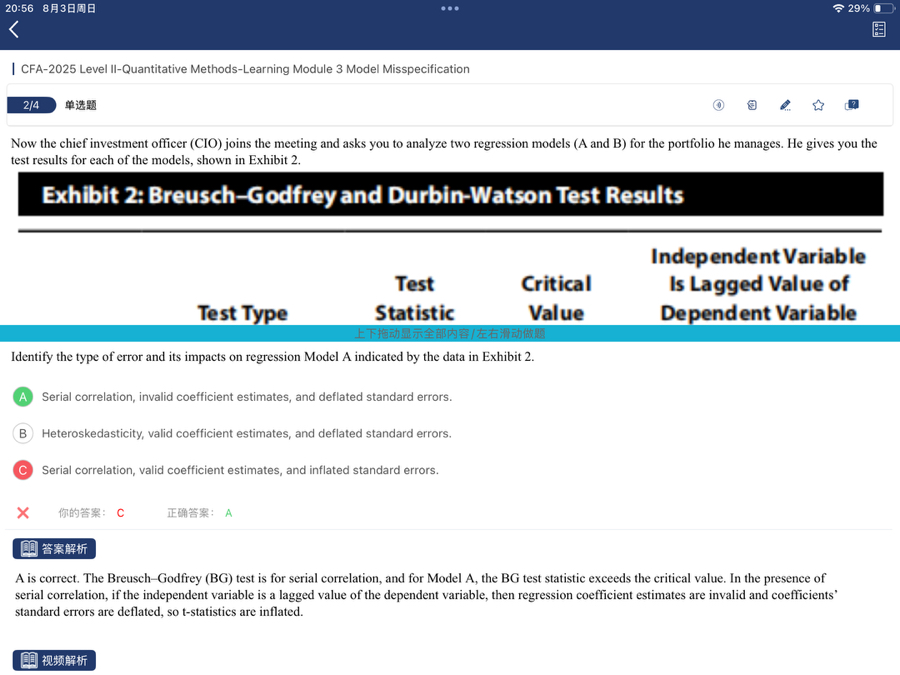

該題答案和解析都說明序列相關會導致coefficience無效,為什么基礎課程中顯示coefficience不被影響

查看更多

查看更多

151****7750

提問

14

上次登錄

1小時前